Futures Market: Overnight, LME copper opened at $9,408/mt, briefly dipping to $9,406.5/mt at the start of trading. It then fluctuated upward within a wide range, peaking at $9,467/mt near the session's end and closing at $9,453/mt, up 0.14%. Trading volume reached 19,000 lots, and open interest stood at 288,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 77,410 yuan/mt. After a slight upward movement at the start, it trended lower, hitting a low of 77,330 yuan/mt. It then fluctuated upward to a high, maintaining rangebound fluctuations near the session's end and peaking at 77,650 yuan/mt before pulling back slightly to close at 77,570 yuan/mt, up 0.22%. Trading volume reached 22,000 lots, and open interest stood at 181,000 lots.

【SMM Copper Morning Brief】News: (1) US aluminum and steel stocks rose as Trump announced plans to impose a 25% tariff on all steel and aluminum imports into the US. The S&P Composite 1500 Steel Index surged by as much as 5.5%, marking the largest intraday gain since November last year. (2) On February 10, Premier Qiang Li chaired a State Council executive meeting to discuss measures to boost consumption, approve the "2025 Action Plan for Stabilizing Foreign Investment," and address structural imbalances in key industries. The meeting emphasized that boosting consumption is a top priority for expanding domestic demand and strengthening the domestic economic cycle.

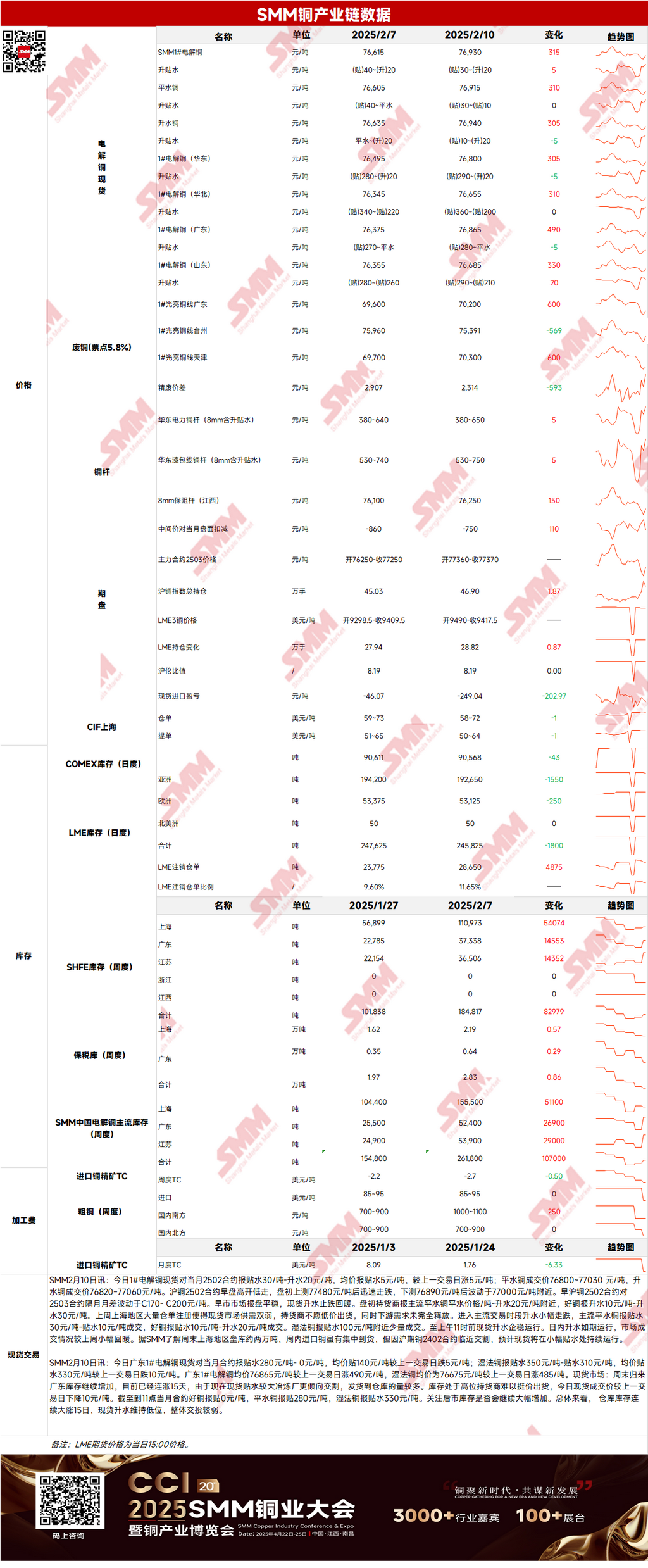

Spot Market: (1) Shanghai: On February 10, #1 copper cathode spot prices against the front-month 2502 contract were quoted at a discount of 30 yuan/mt to a premium of 20 yuan/mt, with an average price at a discount of 5 yuan/mt, up 5 yuan/mt WoW. Spot premiums performed as expected, with market transactions slightly improving WoW. According to SMM, inventory buildup in Shanghai over the weekend was around 20,000 mt. Although imported copper saw concentrated arrivals during the week, spot prices are expected to remain at slight discounts due to the approaching delivery of the SHFE copper 2402 contract.

(2) Guangdong: On February 10, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 280 yuan/mt to parity, with an average price at a discount of 140 yuan/mt, down 5 yuan/mt WoW. Overall, warehouse inventories have surged for 15 consecutive days, spot premiums remained low, and overall trading activity was weak.

(3) Imported Copper: On February 10, warehouse warrant prices ranged from $58 to $72/mt (QP February), with an average price down $1/mt WoW. B/L prices ranged from $50 to $64/mt (QP March), with an average price down $1/mt WoW. EQ copper (CIF B/L) prices ranged from $3/mt to $17/mt (QP March), with the average price unchanged WoW. Quotes referenced cargoes arriving in mid-to-late February. Yesterday, the price spread between the LME 3M contract and the COMEX most-traded contract approached $800/mt. Tight supply expectations for February, driven by shipments from Asia, Africa, and South America, kept late-month offers firm despite weaker SHFE/LME price ratios and lower transaction centers. Buyers were actively seeking cargoes.

(4) Secondary Copper: On February 10, secondary copper raw material prices rose by 600 yuan/mt WoW. Guangdong bare bright copper prices ranged from 70,100 to 70,300 yuan/mt, up 600 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 2,314 yuan/mt, down 593 yuan/mt WoW. The price difference between primary and secondary copper rods was 1,265 yuan/mt. According to the SMM survey, most secondary copper rod enterprises have resumed normal production and sales. Regionally, shipments from south-west China secondary copper rod enterprises were significantly higher than other regions, mainly due to wire and cable enterprises in south-west China resuming operations at approximately 70%, higher than other regions. The secondary copper industry chain is expected to return to normal operating levels after the Lantern Festival.

(5) Inventory: On February 10, LME copper cathode inventories decreased by 1,800 mt to 245,825 mt. SHFE warrant inventories increased by 15,196 mt to 68,204 mt.

Prices: Macro side, the US dollar index hovered at highs as Trump pledged to impose a 25% tariff on all steel and aluminum imports, limiting copper price gains. Tonight, Fed Chairman Jerome Powell will attend a hearing and deliver his semi-annual monetary policy testimony, which could be a key factor influencing expectations for US Fed interest rate cuts. Fundamentals side, copper prices remained strong, with relatively limited spot supply and slightly improved spot market trading sentiment WoW. As of Monday, February 10, SMM data showed copper inventories in major regions across China increased by 31,700 mt WoW to 304,800 mt, up 139,000 mt from pre-holiday levels. Among them, Shanghai inventories were up 71,100 mt, Guangdong up 37,400 mt, and Jiangsu up 29,000 mt compared to pre-holiday levels. Price-wise, Trump's tariff policy continues to disrupt the market significantly. While expectations for the US Fed to hold rates steady in March have strengthened, current market reactions suggest copper prices are likely to remain relatively stable today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make cautious decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】